Weekly Outlook

What Happened This Week?

Global

● The International Monetary Fund warned that renewed U.S.-Iran hostilities have reduced the global economy’s ability to absorb another energy shock.

● The initial impact on energy markets has been contained by higher production from other oil exporters and the release of strategic reserves.

● The IMF cautioned that global growth could fall below its current 3.0% forecast for 2026 if the Middle East conflict escalates further.

Eurozone

● Eurozone industrial production declined 0.2% in May, ending a three-month period of resilient activity.

● The result missed expectations for a modest increase.

● Weaker output of durable consumer goods weighed on production.

● Declines in France, Italy and Ireland more than offset stronger performance elsewhere in the bloc.

United Kingdom

● Bank of England Governor Andrew Bailey warned that renewed fighting between the U.S. and Iran highlights ongoing geopolitical risks.

● Bailey said the impact of higher energy prices on U.K. inflation has remained limited so far.

● U.K. inflation held at 2.8% in May, remaining above the Bank of England’s 2% target.

China

● China’s economy grew 4.3% year-over-year in the second quarter, marking its weakest expansion since late 2022.

● Strong exports linked to AI demand continued to support growth.

● Weak domestic consumption and a prolonged property downturn remained major drags on the economy.

● Property investment fell 18% in the first half of the year compared with the same period in 2025.

● Sluggish domestic demand continued to pressure corporate profits and employment, pushing more workers toward temporary and gig-economy jobs.

South Korea

● The Bank of Korea raised its benchmark interest rate by 25 basis points to 2.75%.

● Policymakers signaled additional rate increases are likely as inflation and economic growth remain stronger than expected.

● The move was widely anticipated by financial markets.

Canada

● The Bank of Canada left its policy rate unchanged at 2.25% for a sixth consecutive meeting.

● Governor Tiff Macklem said second-quarter growth is expected to strengthen.

● Macklem warned that prolonged high energy prices could gradually spread inflation beyond the energy sector.

● Manufacturing shipments increased 1.3% in May to a record high, led by transportation equipment and chemicals.

● Wholesale trade was broadly unchanged after three consecutive months of growth.

● A KPMG Canada survey found that more than half of manufacturers have delayed or reduced investment plans because of trade uncertainty.

United States

● U.S. producer prices fell 0.3% in June as lower energy costs reduced wholesale inflation.

● Federal Reserve Chair Kevin Warsh reaffirmed the Fed’s commitment to bringing inflation back under control.

● Warsh continued to avoid providing guidance on future interest-rate decisions and stressed that monetary policy will remain independent from political influence.

● The share of unemployed Americans out of work for more than six months rose to 27.3%, close to its highest level since 2021.

● Long-term unemployment has increasingly affected white-collar and prime-age workers.

● Analysts said subdued hiring continues to make it more difficult for unemployed workers to return to the labor market.

● Pending home sales fell 5.4% in June, significantly below expectations.

● Higher mortgage rates and record home prices continued to weigh on housing demand.

● Pending home sales declined across every U.S. region, with the Midwest posting the sharpest drop.

● Initial jobless claims declined to 208,000, remaining consistent with a resilient labor market.

● Continuing unemployment claims also edged lower to 1.81 million.

New Zealand

● The Reserve Bank of New Zealand warned that businesses are passing higher costs on to consumers more quickly than in previous years.

● Policymakers are increasingly concerned that inflation could remain elevated even if input costs begin to ease.

● Following last week’s rate increase, economists expect further policy tightening in the coming months.

This Week’s Market Movers

Forex

● The EUR/RUB is up more than 3%.

● The USD/RUB is up more than 2.9%.

● The NZD/CHF is up more than 1.60%.

● The NZD/USD is up more than 1.40%.

● The JPY/NZD is down more than 1.40%.

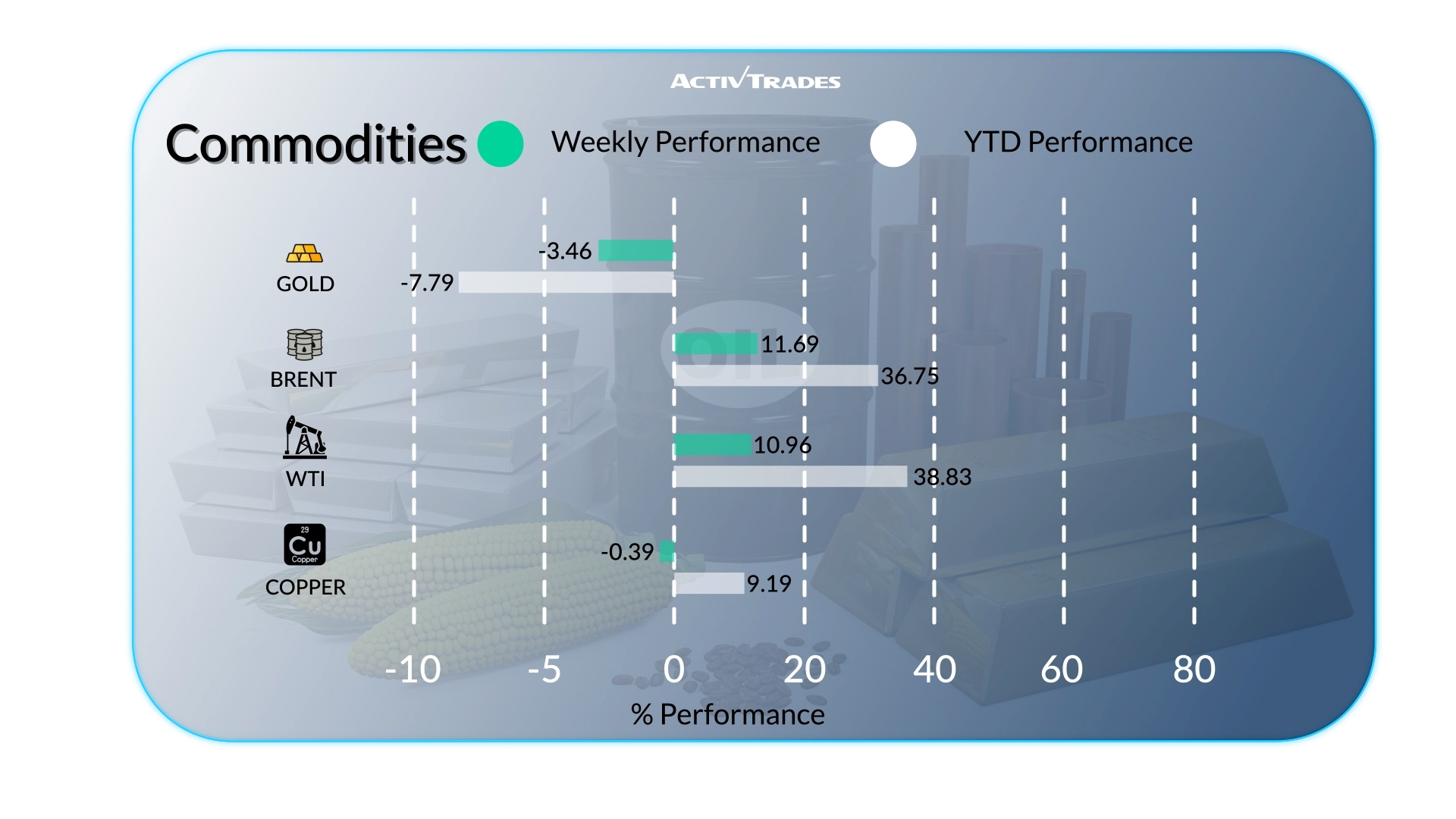

Commodities

● Oats and London Gas Oil prices are up more than 13%.

● Brent and Crude Oil prices are up more than 11.50%.

● Cocoa prices are down more than 10%.

● Orange juice prices are down more than 8.5%.

● Silver prices are down more than 7.5%.

Indices

● The IDX 30 index is up more than 4.5%.

● The Bovespa index is up more than 1.8%.

● The KOSPI index is down more than 8.5%.

● The Japan 225 index is down more than 7%.

Shares

Tops

● PayPal: +29.31%

● CSN Mineracao: +17.20%

● Vodafone Group Public: +19.18%

● Cintas: +15.74%

● Meta Platforms: +13.79%

● Intuit: +13.11%

● Thomson Reuters: +13.05%

● Stellantis: +11.86%

● Palo Alto Networks: +11.20%

● ICG: +11.07%

● QIAGEN: +10.19%

Flops

● Alnylan Pharmaceuticals: -25.19%

● Nebius: -25.05%

● Marvell Technology: -23.51%

● Astera Labs: -23.48%

● International Business Machines: -23.36%

● Sandisk: -23.13%

● Rocket Lab: -21.95%

● Coreweave: -21.88%

● Western Digital: -21.43%

● Seagate Technology: -19.17%

● St. James Place: -11.94%

● Infineon Technologies: -11.32%

Important Events to Follow

Monday 20 July

● 12:30 PM - Canadian - Inflation Rate YoY (June)

○ Previous: 3.2%

○ Forecast: 3%

Tuesday 21 July

● 06:00 AM - UK - Unemployment Rate (May)

○ Previous: 4.9%

○ Forecast: 4.9%

● 09:00 AM - German - ZEW Economic Sentiment Index (July)

○ Previous: 10.5

○ Forecast: 7

● 11:50 PM - Japanese - Balance of Trade (June)

○ Previous: ¥-378.7B

○ Forecast: ¥ -700B

Wednesday 22 July

● 06:00 AM - UK - Inflation Rate YoY (June)

○ Previous: 2.8%

○ Forecast: 2.4%

Thursday 23 July

● 12:15 PM - European - Deposit Facility Rate

○ Previous: 2.25%

○ Forecast: 2.25%

● 12:15 PM - European - ECB Interest Rate Decision

○ Previous: 2.40%

○ Forecast: 2.4%

● 12:45 PM - European - ECB Press Conference

● 11:00 PM - Australian - S&P Global Manufacturing PMI Flash (July)

○ Previous: 51.5

○ Forecast: 51.1

● 11:00 PM - Australian - S&P Global Services PMI Flash (July)

○ Previous: 50.5

○ Forecast: 50.2

● 11:00 PM - Australian - S&P Global Composite PMI Flash (July)

○ Previous: 50.4

○ Forecast: 50.1

● 11:30 PM - Japanese - Inflation Rate YoY (June)

○ Previous: 1.5%

○ Forecast: 1.7%

Friday 24 July

● 12:30 AM - Japanese - S&P Global Manufacturing PMI Flash (July)

○ Previous: 54.8

○ Forecast: 54.3

● 12:30 AM - Japanese - S&P Global Services PMI Flash (July)

○ Previous: 52.2

○ Forecast: 53

● 12:30 AM - Japanese - S&P Global Composite PMI Flash (July)

○ Previous: 52.8

○ Forecast: 52.8

● 06:00 AM - German - GfK Consumer Confidence (August)

○ Previous: -29.2

○ Forecast: -30

● 06:00 AM - UK - Retail Sales MoM (June)

○ Previous: 1.2%

○ Forecast: 0.3%

● 07:15 AM - French - S&P Global Composite PMI Flash (July)

○ Previous: 47.2

○ Forecast: 48.4

● 07:15 AM - French - S&P Global Manufacturing PMI Flash (July)

○ Previous: 51.2

○ Forecast: 50.9

● 07:15 AM - French - S&P Global Services PMI Flash (July)

○ Previous: 46.8

○ Forecast: 47.9

● 07:30 AM - German - S&P Global Manufacturing PMI Flash (July)

○ Previous: 50.3

○ Forecast: 49.5

● 07:30 AM - German - S&P Global Composite PMI Flash (July)

○ Previous: 49.5

○ Forecast: 50

● 07:30 AM - German - S&P Global Services PMI Flash (July)

○ Previous: 48.6

○ Forecast: 49.1

● 08:00 AM - European - S&P Global Composite PMI Flash (July)

○ Previous: 50.0

○ Forecast: 50.2

● 08:00 AM - European - S&P Global Manufacturing PMI Flash (July)

○ Previous: 51.4

○ Forecast: 51

● 08:00 AM - European - S&P Global Services PMI Flash (July)

○ Previous: 49.4

○ Forecast: 50

● 08:30 AM - UK - S&P Global Manufacturing PMI Flash (July)

○ Previous: 52.5

○ Forecast: 52

● 08:30 AM - UK - S&P Global Services PMI Flash (July)

○ Previous: 48.8

○ Forecast: 49.3

● 08:30 AM - UK - S&P Global Composite PMI Flash (July)

○ Previous: 49.3

○ Forecast: 49.7

● 01:45 PM - American - S&P Global Composite PMI Flash (July)

○ Previous: 51.9

○ Forecast: 51.5

● 01:45 PM - American - S&P Global Manufacturing PMI Flash (July)

○ Previous: 53.9

○ Forecast: 53

● 01:45 PM - American - S&P Global Services PMI Flash (July)

○ Previous: 51.2

○ Forecast: 51

Major Earnings Reports to Watch

Tuesday 21 July

● UCB

● 3M

● Halliburton

● Hasbro

● General Motors

● Novartis

● Julius Baer

Wednesday 22 July

● Alphabet

● TESLA MOTORS

● AT&T

● IBM

● Philip Morris

● Banco Santander

● Iberdrola

● Moncler

● Valeo

Thursday 23 July

● Eurofins Scientific

● Total

● Raytheon Technology

● Newmont Goldcorp

● Lockheed Martin

● American Airlines

● INTEL

● Union Pacific

● STMicro

● SAP

● Nokia Corp

● Dassault Systemes

● T-Mobile US

● BNP Paribas

● Repsol

● Unicredit

● Roche

● RELX

● Carrefour

● Nestle

Friday 24 July

● Volkswagen

● AMERICAN EXPRESS

● VERIZON

● Banco de Sabadell

● Poste Italiane

Source: The Wall Street Journal, Investing, Trading Economics, Reuters, TradingView and ActivTrades’ Data as of July 17, 2026

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk.