Weekly Outlook

What Happened This Week?

Global

● Fitch lowered its 2026 global growth forecast to 2.4%, citing the economic impact of higher oil prices and ongoing disruptions in the Middle East.

● The agency raised its average Brent crude forecast for 2026 to $87 per barrel from $70 due to concerns over prolonged shipping disruptions in the Strait of Hormuz.

● The OECD warned that elevated energy costs could significantly slow global activity next year.

● OECD projections suggest global growth could reach 2.8% if energy supply conditions improve, but a prolonged conflict could drag growth down to just 2.1%.

● China was one of the few economies to receive an upgraded outlook, with growth expected at 4.6% in 2026, supported by strong AI-related investment.

United States

● Several Federal Reserve officials signaled growing concern that inflation may remain too high, increasing the possibility of additional rate hikes later this year.

● Interest-rate futures now imply a much higher probability of policy tightening compared with one month ago.

● Businesses reported rising energy-related costs and continued uncertainty linked to geopolitical tensions.

● Economic conditions remain uneven, with higher-income households continuing to spend while lower-income consumers face increasing financial pressure.

● The ISM services index rose to 54.5 in May, indicating stronger-than-expected expansion in the services sector.

● Service-sector companies reported the fastest price increases in nearly three years, largely driven by fuel and transportation costs.

● Manufacturing activity expanded for a fifth consecutive month, supported by solid production and new orders.

● Construction spending exceeded expectations in April, with gains in both residential and public-sector projects.

● Initial jobless claims increased modestly, suggesting some softening in labor-market conditions.

● ADP reported private-sector job creation of 122,000 positions in May, pointing to continued labor-market resilience.

● Technology companies continued to reduce headcount, with AI-related restructuring cited as a leading reason for layoffs.

● Consumer surveys showed growing financial anxiety as households face higher food, fuel and borrowing costs.

Eurozone

● Inflation accelerated to 3.2% in May, its highest level since 2023, mainly due to rising energy costs.

● Markets increasingly expect the ECB to raise interest rates at its June meeting.

● The ECB upgraded its inflation forecasts and policymakers continue to emphasize inflation risks.

● Retail sales contracted more than expected in April, reflecting weaker consumer spending.

● Consumer confidence remains close to historic lows and economists increasingly see recession risks for the second quarter.

● Manufacturing companies reported the strongest increase in input costs since 2022.

● Services activity weakened sharply, highlighting the growing impact of higher energy prices on the economy.

● Factory job losses accelerated during May.

● Household inflation expectations remained elevated, while expectations for wage growth declined.

● Despite economic weakness, the unemployment rate held steady at 6.3%.

United Kingdom

● Bank of England policymaker Megan Greene suggested that the case for higher interest rates has strengthened.

● Concerns are growing that inflation expectations could become entrenched if policymakers delay action.

● Some BOE officials remain cautious given the fragile state of economic growth.

Japan

● Bank of Japan Governor Kazuo Ueda indicated that additional rate increases remain possible if inflation pressures continue to build.

● Policymakers highlighted rising wages, elevated oil prices and negative real interest rates as factors supporting tighter policy.

● Markets are pricing a high probability of a BOJ rate hike in the near term.

● The yen remains weak despite significant government intervention in the currency market.

● Japanese authorities reiterated their readiness to act again if currency volatility intensifies.

Canada

● Canada’s services sector returned to expansion territory in May after several months of contraction.

● GDP declined slightly during the first quarter, marking a second consecutive quarterly contraction.

● Weak growth has increased concerns about a potential recession, although economists remain divided on the outlook.

● Business sentiment remains pressured by geopolitical uncertainty and external trade challenges.

Australia

● Economic growth slowed to 0.3% during the first quarter, reflecting tighter monetary conditions and higher fuel costs.

● Annual growth remained at 2.5%.

● The Reserve Bank of Australia delivered a third consecutive interest-rate increase in May.

● Business investment remained strong, supported by substantial spending on machinery, equipment and data-center infrastructure.

India

● The Reserve Bank of India left interest rates unchanged for a third consecutive meeting.

● Policymakers maintained a neutral stance while monitoring the economic consequences of Middle East tensions.

● The Indian rupee has weakened sharply this year as higher oil prices increase pressure on the country's import bill.

Switzerland

● Inflation remained stable at 0.6% in May.

● Markets expect the Swiss National Bank to keep rates unchanged through the remainder of the year.

● Policymakers continue to view medium-term inflation trends as broadly stable and within target.

This Week’s Market Movers

Forex

● The USD/RUB and EUR/RUB are up more than 3.5%.

● The GBP/NZD is up more than 1%.

● The NZD/USD and the NZD/HKD are down more than 1%.

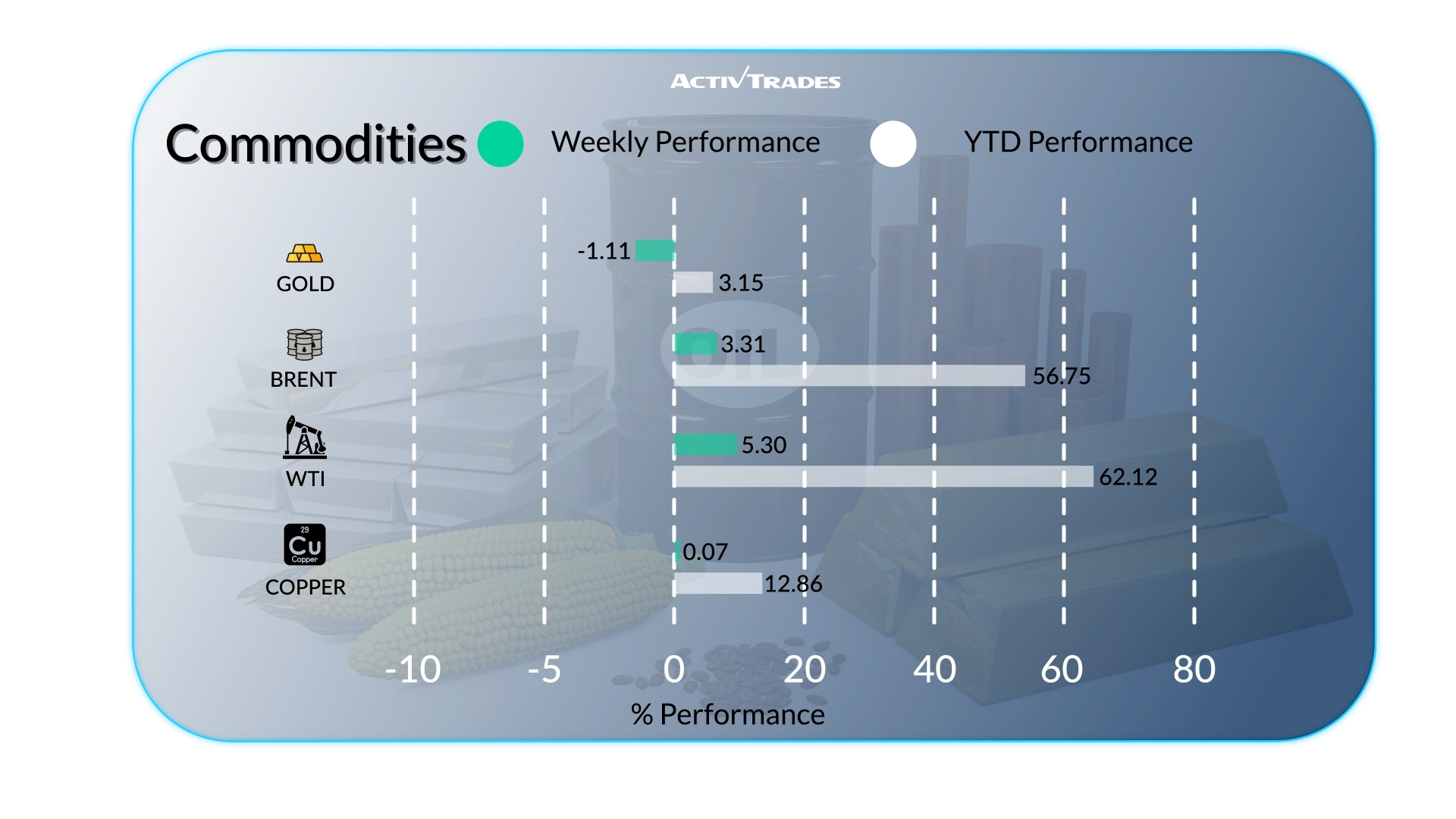

Commodities

Gold:

● WTI prices are up more than 6%.

● Orange Juice prices are up more than 5.8%.

● Brent prices are up more than 3%.

● US Coffee and Oats prices are down more than 6.5%.

● Corn and Palladium prices are down more than 5.5%.

● Silver prices are down more than 5%.

● Soybeans and Weat prices are down more than 4.9%.

Indices

● The Japan 225 index is up more than 2%.

● The Dow index is up more than 1.7%.

● The VIX index is down more than 8%.

● The Bovespa index is down more than 3.5%.

Shares

Tops

● Marvell Technology: +59.21%

● Hewlett Packard: +43.29%

● Dell Technologies: +33.13%

● Axon Enterprise: +30.39%

● ARM: +26.92%

● NetApp: +26.07%

● Super Micro Computer: +23.42%

● Companhia de Saneamento de Minas: +18.58%

● STMicroelectronics: +14.25%

● Rio Tinto: +14.06%

● Infineon Technologies: +10.51%

Flops

● Magazine Luiza: -20.77%

● Braskem: -20.35%

● Cboe Global Markets: -18.02%

● Cosan: -17.51%

● Azzas: -15.79%

● Strategy: -13.16%

● Prudential: -11.66%

Important Events to Follow

Tuesday 09 June

● 12:30 AM - Australian - Westpac Consumer Confidence Change (June)

○ Previous: 3.5%

○ Forecast: -1.2%

● 01:30 AM - Australian - NAB Business Confidence (May)

○ Previous: -24

○ Forecast: -22

● 03:00 AM - Chinese - Balance of Trade (May)

○ Previous: $84.82B

○ Forecast: $89.0B

● 03:00 AM - Chinese - Exports YoY (May)

○ Previous: 14.1%

● 03:00 AM - Chinese - Imports YoY (May)

○ Previous: 25.3%

● 06:00 AM - German - Balance of Trade (May)

○ Previous: €14.3B

○ Forecast: €13.6B

● 02:00 PM - American - Existing Home Sales (May)

○ Previous: 4.02M

○ Forecast: 3.9M

Wednesday 10 June

● 01:30 AM - Chinese - Inflation Rate YoY (May)

○ Previous: 1.2%

○ Forecast: 1.4%

● 12:30 PM - American - Core Inflation Rate YoY (May)

○ Previous: 2.8%

○ Forecast: 2.8%

● 12:30 PM - American - Inflation Rate YoY (May)

○ Previous: 3.8%

○ Forecast: 3.9%

● 01:45 PM - Canadian - BoC Interest Rate Decision

○ Previous: 2.25%

○ Forecast: 2.25%

Thursday 11 June

● 12:15 PM - European - Deposit Facility Rate

○ Previous: 2%

○ Forecast: 2.25%

● 12:15 PM - European - ECB Interest Rate Decision

○ Previous: 2.15%

○ Forecast: 2.4%

● 12:30 PM - American - PPI MoM (May)

○ Previous: 1.4%

○ Forecast: 0.3%

● 12:45 PM - European - ECB Press Conference

Friday 12 June

● 06:00 AM - UK - GDP MoM (April)

○ Previous: 0.3%

○ Forecast: 0.1%

● 02:00 PM - American - Michigan Consumer Sentiment Prel (June)

○ Previous: 44.8

○ Forecast: 46

Major Earnings Reports to Watch

Wednesday 10 June

● Oracle

Thursday 11 June

● ADOBE

Source: The Wall Street Journal, Investing, Trading Economics, Reuters, TradingView and ActivTrades’ Data as of June 05, 2026

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.