Warren Buffett, who many consider to be the greatest investor ever, famously said:

"It’s only when the tide goes out that you discover who's been swimming naked”

At the weekend (02/05/2026), Mr. Buffett gave an interview, in which he talked about the state of play in the financial markets today.

He said that:

“So we’ve never had people in a more gambling mood than now. But that doesn’t mean that investing is terrible. It does mean that prices for an awful lot of things will look very silly.”

Though Warren Buffett doesn't run Berkshire Hathaway (the firm that he and his former partner Charlie Munger created) anymore, having retired as CEO, he remains a significant shareholder in the business, which is sitting on a cash pile approaching $400.0 billion.

In the past, Buffet has used the cash in the business to strike attractive deals and make acquisitions, on advantageous terms, often following a market shakeout or crisis.

Buffett's view seems to be that in some sections of the market, stock prices have become detached from earnings and revenue growth; that is, investors and traders are paying increasingly high multiples for stocks that, in Mr. Buffett's opinion, will never justify those valuations.

Why might Warren Buffett think that?

Let's look at the price-to-sales ratio among S&P 500 stocks as an example.

A stock price that’s 10.0 times higher than the company’s sales or revenue per share has long been considered an extreme valuation that very few, if any, stocks could justify.

However, if we examine the S&P 500 constituents, we find that there are more than 50 stocks in the index with a price-to-sales ratio greater than 10.0 times.

10 of those have a ratio that’s higher than 20 times sales.

And if we look at the Price Earnings or P/E ratio for the blue-chip US index, we find that the S&P 500 currently trades on a 12-month forward PE of 20.90 times earnings.

Yet, more than 200 stocks within the index have a PE greater than 21.0 times; 44 of those are trading at a PE ratio greater than 40.00 times earnings.

It’s possible to try to justify that rating, in some cases.

For example, Palo Alto Networks PANW US has a Forward PE of 83.89 times, but has grown its earnings more than 8.80 times over the last 5 years.

At the same time, sales or revenues at the business have grown by just +170% in that period.

This tells us that Palo Alto is growing its margins on both existing and new business.

In fact, I would go so far as to say that you make the case for PANW being undervalued at current price levels.

And the chartist in me thinks that there could be scope to retest to $220.00 (see below).

A level which was last seen in November 2025. Just before the market became concerned that AI was going to eat the Software as a Service sector’s breakfast, lunch and dinner.

Source:Barchart.com

Ongoing debate

And that's what this debate is all about: the perceptions that investors and traders have of a stock and its prospects determine what those same investors and traders think it's worth and what they will pay to own it.

That view was summed up by someone that Warren Buffett held in high regard, investor, money manager and academic Philip Fisher, who said that:

"The only true test of whether a stock is 'cheap' or 'high' is not its current price in relation to some former price, no matter how accustomed we may have become to that former price, but whether the company’s fundamentals are significantly more or less favourable than the current financial-community appraisal of that stock.”

Source: Philip Fisher

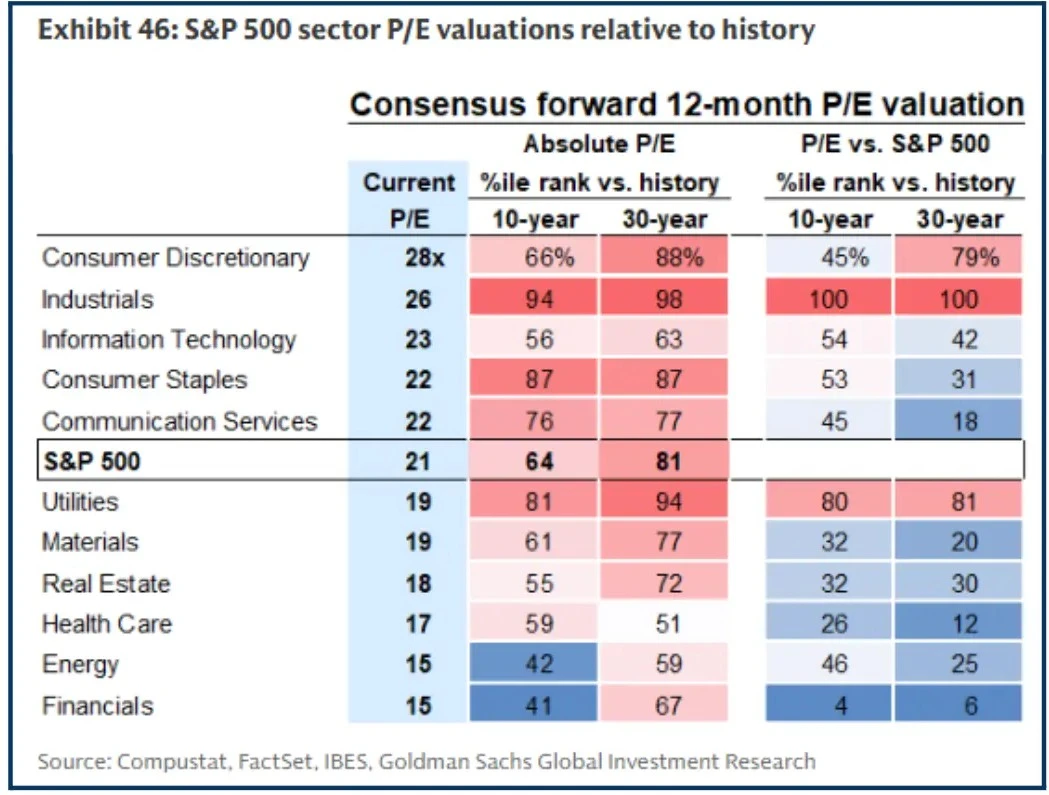

The table below shows the PE ratios for the 11 S&P 500 sectors and the index, as of late April 2026.

It also shows where those PE ratios sat in relation to their 10 and 30-year averages, both outright and relative to the index itself, at the time.

Industrials look expensive on these numbers, whilst financials look undervalued.

Source: GS Research/Mike Zarcadi

Out of the ordinary

We find ourselves in a strange position as far as the markets are concerned.

We have a fragile and skittish macroeconomic and geopolitical background, combined with a very positive earnings season.

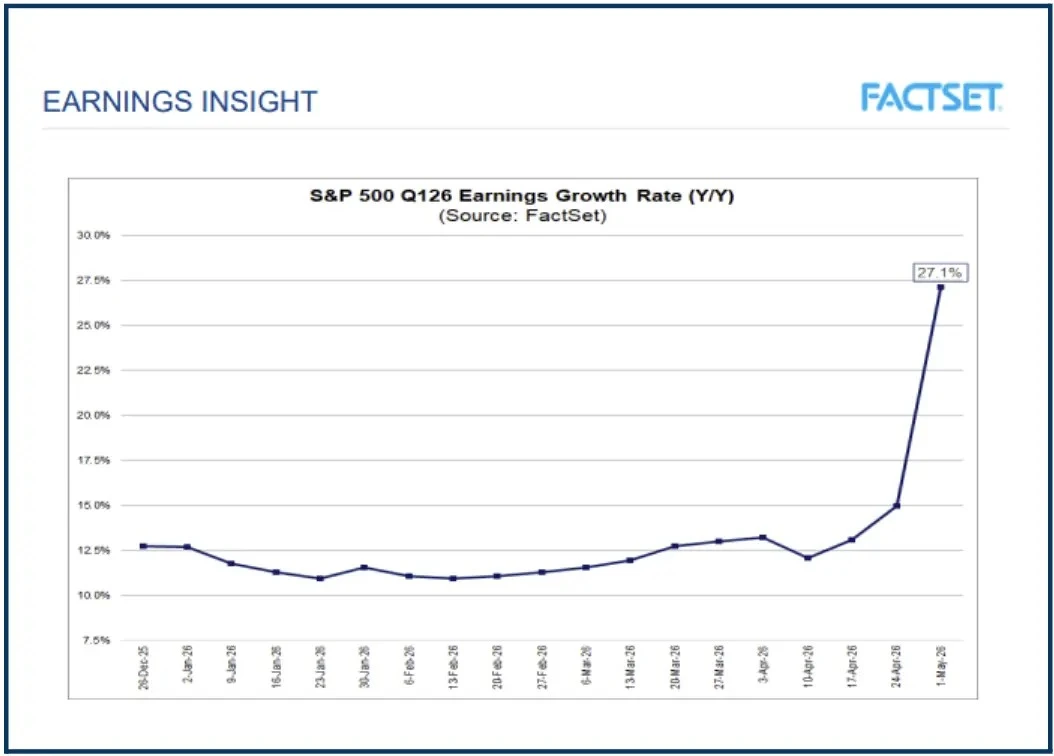

FactSet points out that 10 out of 11 S&P 500 sectors are reporting higher earnings and that 7 sectors are reporting double-digit earnings growth.

And that, following a series of reports from big tech and others, in the final days of April, the earnings growth rate for the quarter has jumped to +27.10 %, the second-highest growth rate since Q4 2021.

Source: Factset Research

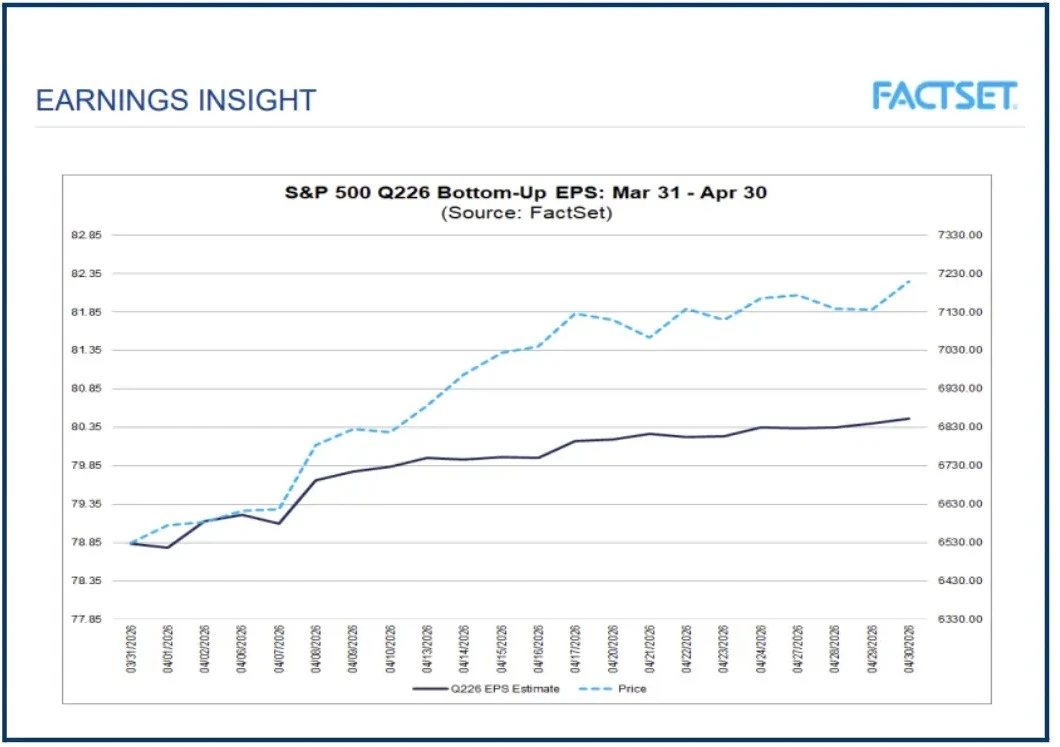

Earnings are growing, and analysts' earnings estimates have been revised higher (dark blue line); however, price (light blue dashed line) has already moved higher and faster in anticipation of this.

Source: Factset Research

What we need to decide now is whether price run too far too fast, as the Buffett camp believes?

Or, if there is more headroom in the market, as stocks like Palo Alto PANW US suggest, is possible?

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.