Weekly Outlook

What Happened This Week?

Global

- The conflict involving Iran is disrupting global energy markets, with the Strait of Hormuz closed and Iran signaling it will use the blockade as leverage against the U.S. and Israel.

- The International Energy Agency warned of the largest oil supply disruption in history, with global supply potentially falling by 8 million barrels per day in March.

- Gulf producers have cut production by around 10 million barrels per day, intensifying supply shortages.

- The IEA plans to release a record 400 million barrels from strategic reserves to stabilize markets.

- Iran warned oil prices could surge to $200 per barrel if the conflict escalates further.

- Surging energy costs are intensifying global inflationary pressures, likely prompting central banks—especially in energy-dependent Asian markets—to adopt more aggressive monetary tightening.

United States

- The Trump administration launched new trade investigations under Section 301 targeting excess industrial capacity in several Asian economies.

- To alleviate supply constraints, the U.S. issued a temporary waiver allowing for the purchase of Russian oil currently held in offshore transit.

- Inflation data continues to send mixed signals: CPI rose 2.4% year-over-year in February, while the Fed’s preferred PCE measure was 2.9% in January.

- The divergence between CPI and PCE largely reflects different weightings for housing and healthcare.

- Initial jobless claims fell to 213,000 in the week through March 7, while continuing claims declined to 1.85 million, indicating layoffs remain limited.

- The U.S. trade deficit narrowed to $54.5 billion in January, a 25% drop from December, as exports rose 5.5% and imports declined 0.7%.

- Capitalizing on a temporary window of lower borrowing costs, buyers pushed existing-home sales up 1.7% to an annualized pace of 4.09 million this February.

- The median existing-home price increased 0.3% year-over-year to $398,000, while mortgage rates moved back above 6% following the Iran conflict.

China

- China’s exports surged 21.8% to $657 billion in January and February, pushing the trade surplus close to $214 billion.

- Exports to the United States fell 11% during the same period, although a recent U.S. court decision striking down tariffs could improve China’s export outlook.

- Beijing maintained its 2026 growth target at 4.5%–5% and pledged to boost domestic demand, though no major new stimulus measures were announced.

Japan

- Japan’s economy grew 1.3% annualized in the fourth quarter of 2025, significantly above the preliminary estimate of 0.2%.

- Strong capital spending supported growth and strengthened the case for further Bank of Japan rate hikes.

- Policymakers face increasing uncertainty as rising oil prices and Middle East tensions complicate the outlook.

Germany

- German manufacturing orders plunged 11.1% in January, with domestic orders falling 16.2% and foreign orders down 7.1%.

- Industrial production declined 0.5% in January after a 1.0% drop in December, highlighting continued weakness in the industrial sector.

- German exports fell 2.3% in January, though shipments to the United States increased 11.7%, making it the country’s largest export destination.

- Germany’s trade surplus widened to €21.2 billion from €17.1 billion the previous month.

- Leading economic institutes lowered Germany’s 2026 growth forecast to around 0.8%–0.9%, citing higher energy prices and global uncertainty.

- Economists say Germany’s recovery is currently driven mainly by fiscal stimulus rather than export growth.

Eurozone

- Economists say the current energy shock differs from the 2022 crisis because weaker consumer demand may offset some inflation pressure.

- Some analysts believe central banks in Europe could lean toward looser policy rather than aggressive tightening if growth weakens.

Canada

- A 4.7% contraction in exports drove Canada’s merchandise trade deficit to C$3.65 billion in January, its widest level since late last year.

- Shipments of motor vehicles, metals, and aircraft declined significantly during the month.

- Canada’s trade surplus with the United States narrowed to C$5.4 billion, while its deficit with other trading partners expanded.

- The housing outlook remains weak: housing starts are expected to decline between 2026 and 2028 due to higher costs and weaker demand.

- Unsold housing inventory reached record levels in major cities, and condominium sales in Toronto fell to their lowest level in more than 40 years.

- Existing-home sales are nearly 20% below year-ago levels and prices remain about 19% below their February 2022 peak.

Turkey

- Turkey’s central bank kept its benchmark one-week repo rate unchanged at 37%.

- Policymakers signaled they may raise interest rates again if higher energy prices push inflation higher.

Singapore

- Singapore rejected U.S. trade data suggesting a $27 billion surplus with the United States in 2024, citing U.S. statistics that instead show a trade deficit.

Thailand

- Thai officials noted that the country’s $51 billion trade surplus with the United States partly reflects exports from U.S. companies operating manufacturing facilities in Thailand.

This Week’s Market Movers

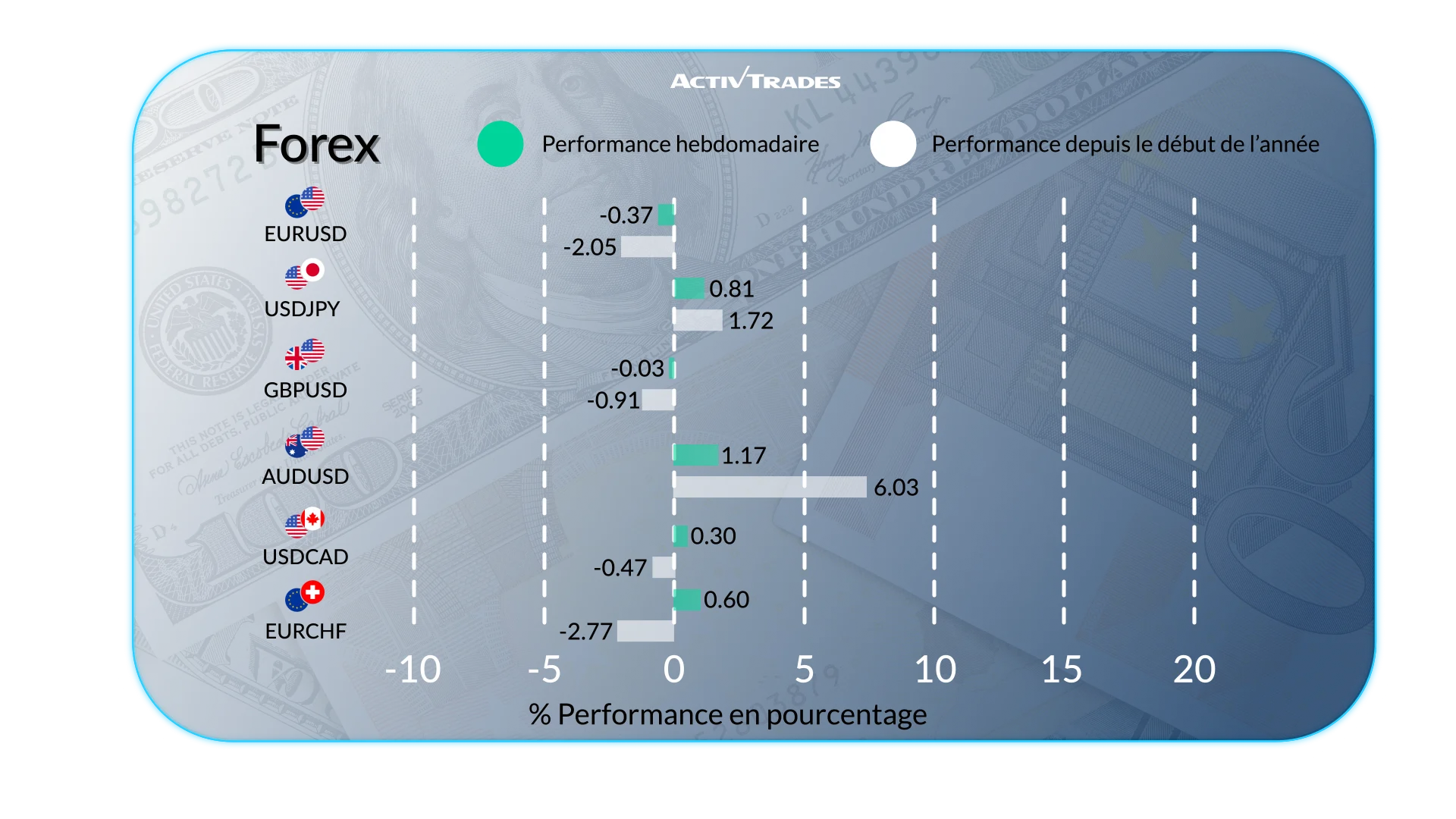

Forex

- The Japanese Yen reached levels inseen in around 40 years.

- The NZD/USD is down more than 1.25%.

- The AUD/NZD is up more than 2.10%.

- The AUD/EUR is up more than 1.90%.

- The JPY/AUD is down more than 1.75%.

- The USD/HUF is up more than 2.10%.

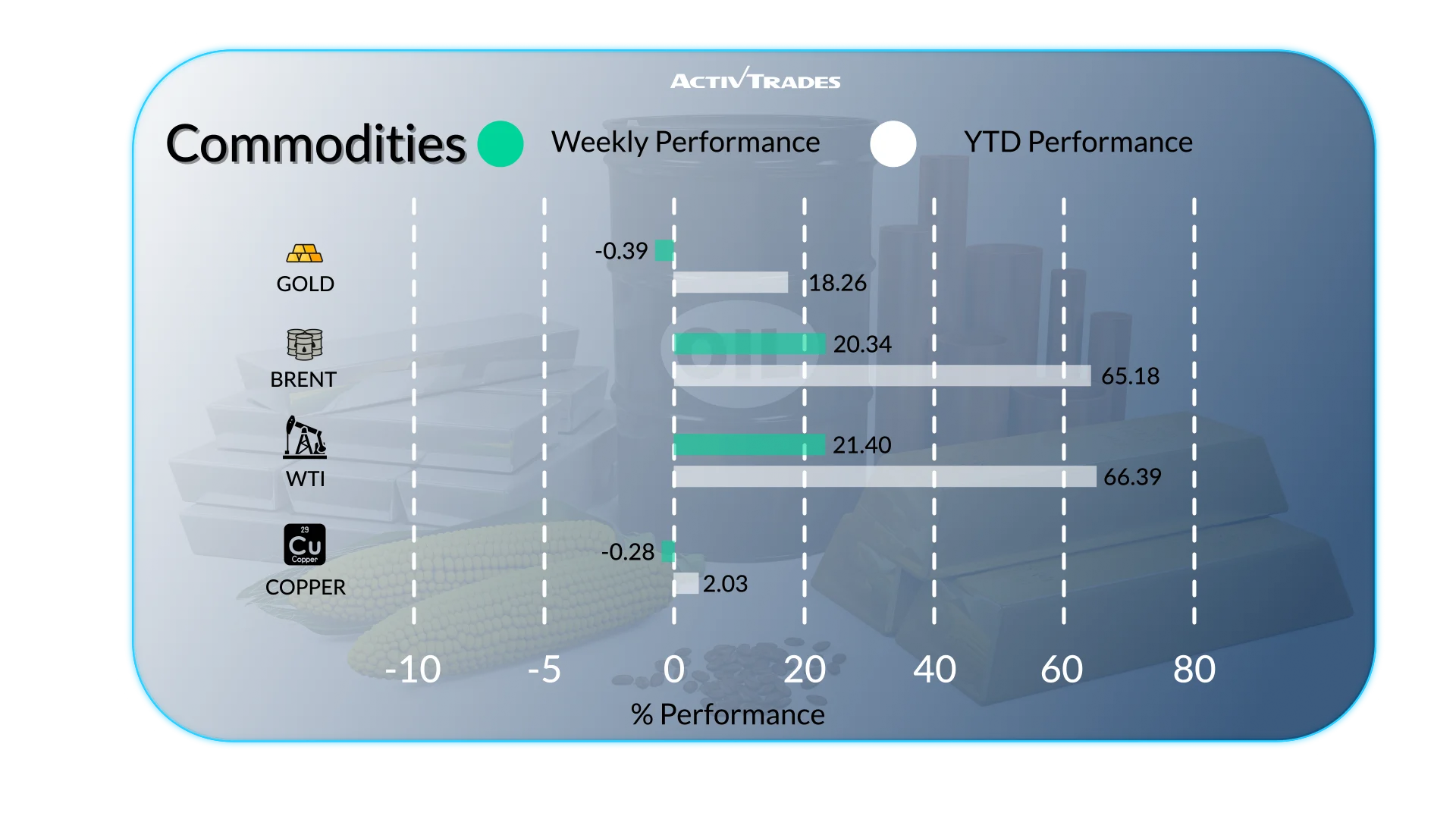

Commodities

- Orange Juice prices are up more than 11%.

- Brent prices are up more than 8% and Crude prices are up around 5%.

- Heating oil prices are up almost 8%.

Indices

- The VIX index is up more than 23%.

- The Dow Jones index is down more than 3.80%

- The Bovespa index is down more than 3.20%.

- The S&P500 index is down more than 2.60%.

- The UK100 index is down more than 2.45%.

- The DAX 40 index is down more than 2.30%.

- The Euro50 index is down more than 2%.

Shares

Tops

- CF Industries Holdings: +28.30%

- Mozaic Company: +20.62%

- LyondellBasell Industries: +16.14%

- Admiral: +12.52%

- Dow: +12.18%

- Zalando: +12.06%

- Petroleo Brasileiro: +12.59%

- Braskem: +11.93%

- Kroger: +11.46%

- Marvell Technology: +11.12%

Flops

- Fair Isaac: -25.16%

- Raizen: -24.59%

- Companhia Siderurgica Nacional: -23.46%

- Centene: -22.51%

- Paramount Skydance: -18.74%

- Old Dominion Freight Line: -17.41%

- Ares Management: -16.79%

- Southwest Airlines: -16.52%

- Trade Desk: -15.76%

- Merck: -13.34%

- Barratt Redrow: -13.24%

Important Events to Follow

Monday 16 March

- 02:00 AM - Chinese - Industrial Production YoY (January-February)

- Previous: 5.2%

- Forecast: 5.1%

- 02:00 AM - Chinese - Retail Sales YoY (January-February)

- Previous: 0.9%

- Forecast: 2.5%

- 12:30 PM - Canadian - Inflation Rate YoY (February)

- Previous: 2.3%

- Forecast: 2.1%

Tuesday 17 March

- 03:30 AM - Australian - RBA Interest Rate Decision

- Previous: 3.85%

- Forecast: 3.85%

- 10:00 AM - German - ZEW Economic Sentiment Index (March)

- Previous: 58.3

- Forecast: 55

- 11:50 PM - Japanese - Balance of Trade (February)

- Previous: ¥-1152.7B

- Forecast: ¥600.0B

Wednesday 18 March

- 12:30 PM - American - PPI MoM (February)

- Previous: 0.5%

- Forecast: 0.3%

- 01:45 PM - Canadian - BoC Interest Rate Decision

- Previous: 2.25%

- Forecast: 2.55%

- 06:00 PM - American - Fed Interest Rate Decision

- Previous: 3.75%

- Forecast: 3.75%

- 06:00 PM - American - FOMC Economic Projections

- 06:30 PM - American - Fed Press Conference

Thursday 19 March

- 03:00 AM - Japanese - BoJ Interest Rate Decision

- Previous: 0.75%

- Forecast: 0.75%

- 07:00 AM - UK - Unemployment Rate (January)

- Previous: 5.2%

- Forecast: 5.2%

- 08:30 AM - Swiss - SNB Interest Rate Decision

- Previous: 0%

- Forecast: 0%

- 12:00 PM - UK - BoE Interest Rate Decision

- Previous: 3.75%

- Forecast: 3.75%

- 01:15 PM - European - Deposit Facility Rate

- Previous: 2%

- Forecast: 2%

- 01:45 PM - European - ECB Press Conference

Major Earnings Reports to Watch

Monday 16 March

- Dollar Tree

Wednesday 18 March

- Weibo Corporation

- Micron Technology

- General Mills

- Jeronimo Martins

Thursday 19 March

- Sonae

- Accenture

- Alibaba

- Enel

Source: The Wall Street Journal, Investing, Trading Economics, Reuters, TradingView and ActivTrades’ Data as of March 13, 2026

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.