Weekly Outlook

What Happened This Week?

United States

● Gasoline prices rose above $4 per gallon for the first time since 2022, driven by the oil shock

● The Fed held rates steady and signaled a higher bar for future rate cuts

● Jerome Powell said the Fed can look through temporary oil shocks but remains cautious on inflation

● Markets now expect rates to stay on hold as uncertainty rises

● Fed officials warned inflation risks from the Iran conflict may require action if they persist

● The nomination of Kevin Warsh as next Fed chair faces political uncertainty

● Job openings fell to 6.9 million, with hiring at its lowest level since 2020

● Private-sector job growth slowed to 62,000 in March

● Jobless claims fell to 202,000, indicating a still-resilient labor market

● Housing market remains soft, with home-price growth slowing to 0.9% annually

● Mortgage affordability remains under pressure as inflation outpaces home prices

● Japanese firms continue to acquire U.S. homebuilders, taking advantage of relatively stronger market conditions

● The U.S. lifted sanctions on Venezuela, aiming to boost oil supply and investment

● Trade policy adjustments on metals could increase import costs

Eurozone

● Economic sentiment weakened further as the Iran war drives uncertainty

● Inflation rose to 2.5% in March, the highest since early 2025, driven by energy prices

● The ECB raised its inflation forecast and cut growth expectations

● Markets are pricing in multiple rate hikes this year

● The unemployment rate edged higher to 6.2%, with risks to hiring increasing

● Policymakers warned inflation could rise further if energy disruptions persist

Germany

● Economic outlook remains fragile, with sentiment weakening due to energy costs

● Growth expectations for 2026 have been downgraded

United Kingdom

● Shop-price inflation edged higher and is expected to accelerate further

● Consumer confidence dropped to its lowest level in nearly a year

● Food inflation could surge to 9–10% by year-end due to supply disruptions and energy costs

● The Bank of England expects inflation to rise toward 3.5% in coming months

Japan

● Companies agreed to the largest wage increase in 35 years, supporting domestic demand

● Inflation in Tokyo slowed slightly, while industrial output declined

● Economic signals remain mixed, complicating the Bank of Japan’s rate path

● Strong wage growth and corporate sentiment support expectations of a rate hike

● However, rising energy costs and weaker forward sentiment create uncertainty

● Japanese firms continue expanding abroad, particularly in U.S. housing

China

● Growth remains under pressure from external risks and weaker global demand

● Policy focus remains on supporting domestic demand amid uncertainty

India

● The economy faces downside risks from the Middle East conflict

● The central bank imposed limits on currency positions to stabilize the rupee

● Growth forecasts may be revised lower due to rising global risks

South Korea

● The won weakened to its lowest level since 2009 against the dollar

● Strong capital inflows helped maintain dollar liquidity despite currency pressure

Canada

● GDP growth remained modest but positive in early 2026

● Economic activity is supported by energy and construction sectors

● The Bank of Canada held rates steady, balancing inflation risks and growth concerns

● Policymakers face increasing difficulty due to higher energy prices and trade uncertainty

Global

● The Iran conflict continues to drive higher energy prices and global uncertainty

● Inflation pressures are rising again, complicating central bank strategies

● Diverging sentiment indicators highlight uncertainty in consumer outlook

● Central banks globally are leaning toward caution, with many pausing or considering tightening depending on inflation trends

This Week’s Market Movers

Forex

● The AUD/NZD and the ZAR/JPY are up more than 1.30%.

● The USD/NOK is up more than 0.60%.

● The GBP/HUF is down more than 1.90%.

● The GBP/ZAR is down more than 1.60%.

● The NZD/JPY is down more than 1%.

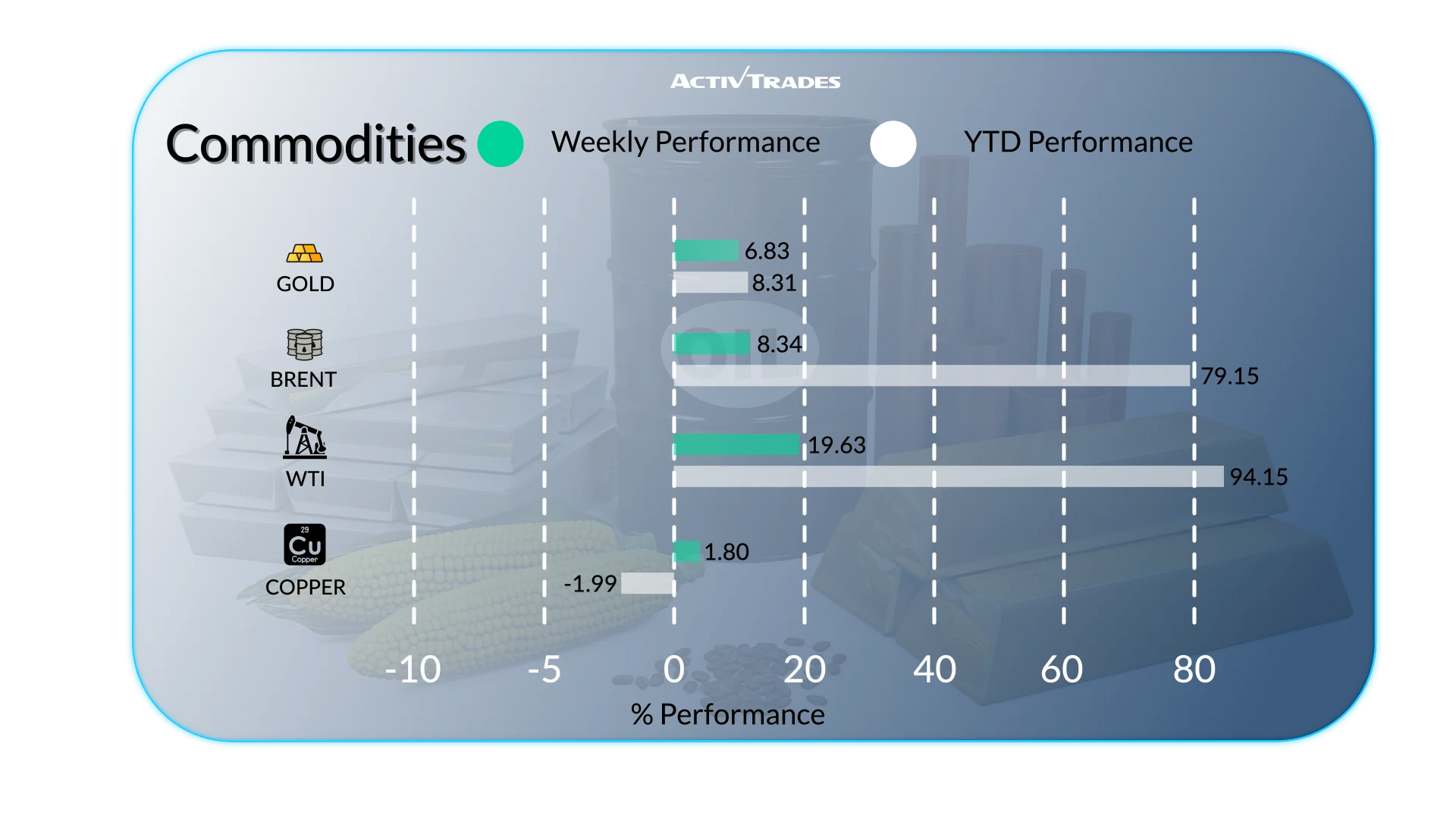

Commodities

● Light Crude Oil prices are up almost 13%.

● Orange Juice prices are up almost 12%.

● London Gas Oil prices are up more than 10%.

● Palladium prices are up more than 7.80%.

● Natural Gas prices are down more than 9.50%.

● US Sugar prices are down more than 5%.

Indices

● The Ita40 index is up more than 4%.

● The UK100 index is up more than 3%.

● The CAC40 index is up more than 2%.

● The VIX index is down more than 9.85%.

Shares

Tops

● SBA Communications: +23.98%

● FacSet Research Systems: +17.52%

● Newmont: +15.21%

● Brown-Foreman: +14.66%

● Sendas Distribuidora: +13.28%

● Entergy: +12.28%

● Stellantis: +11.42%

● Rio Tinto: +10.35%

Flops

● Compass: -98.64%

● Texas Pacific Land: -14.40%

● NIKE: -16.24%

● Braskem: -14.16%

● Sysco: -13.39%

● Strategy: -12.24%

● EQT: -12.04%

Important Events to Follow

Monday 06 April

● 01:30 PM - Canadian - S&P Global Composite PMI (March)

○ Previous: 47.1

○ Forecast: 47.5

● 01:30 PM - Canadian - S&P Global Services PMI (March)

○ Previous: 46.5

○ Forecast: 48

● 02:00 PM - American - ISM Services PMI (March)

○ Previous: 56.1

○ Forecast: 55

● 11:00 PM - Australian - S&P Global Composite PMI Final (March)

○ Previous: 52.4

○ Forecast: 47.00

● 11:00 PM - Australian - S&P Global Services PMI Final (March)

○ Previous: 52.8

○ Forecast: 46.6

Tuesday 07 April

● 07:15 AM - Spanish - S&P Global Services PMI (March)

○ Previous: 51.9

○ Forecast: 51.5

● 07:15 AM - Spanish - S&P Global Composite PMI (March)

○ Previous: 51.5

○ Forecast: 51.3

● 07:50 AM - French - S&P Global Composite PMI Final (March)

○ Previous: 49.9

○ Forecast: 48.3

● 07:50 AM - French - S&P Global Services PMI Final (March)

○ Previous: 49.6

○ Forecast: 48.3

● 07:55 AM - German - S&P Global Composite PMI Final (March)

○ Previous: 53.2

○ Forecast: 51.9

● 07:55 AM - German - S&P Global Services PMI Final (March)

○ Previous: 53.5

○ Forecast: 51.2

● 08:00 AM - European - S&P Global Composite PMI Final (March)

○ Previous: 51.9

○ Forecast: 50.5

● 08:00 AM - European - S&P Global Services PMI Final (March)

○ Previous: 51.9

○ Forecast: 50.1

● 08:30 AM - UK - S&P Global Composite PMI Final (March)

○ Previous: 53.7

○ Forecast: 51

● 08:30 AM - UK - S&P Global Services PMI Final (March)

○ Previous: 53.9

○ Forecast: 51.2

● 12:30 PM - American - Durable Goods Orders MoM (February)

○ Previous: 0%

○ Forecast: 0.6%

● 02:00 PM - Canadian - Ivey PMI s.a (March)

○ Previous: 56.6

○ Forecast: 51

Wednesday 08 April

● 07:30 AM - European - HCOB Construction PMI (March)

○ Previous: 46.0

○ Forecast: 46.6

● 07:30 AM - French - HCOB Construction PMI (March)

○ Previous: 43.9

○ Forecast: 45

● 07:30 AM - German - HCOB Construction PMI (March)

○ Previous: 43.7

○ Forecast: 44.5

● 08:30 AM - UK - S&P Global Construction PMI (March)

○ Previous: 44.5

○ Forecast: 47

● 06:00 PM - American - FOMC Minutes

Thursday 09 April

● 05:00 AM - Japanese - Consumer Confidence (March)

○ Previous: 40.0

○ Forecast: 38

● 06:00 AM - German - Balance of Trade (February)

○ Previous: €21.2B

○ Forecast: €19.1B

● 12:30 PM - American - Core PCE Price Index MoM (February)

○ Previous: 0.4%

○ Forecast: 0.4%

● 12:30 PM - American - GDP Growth Rate QoQ Final (Q4)

○ Previous: 4.4%

○ Forecast: 0.7%

● 12:30 PM - American - Personal Income MoM (February)

○ Previous: 0.4%

○ Forecast: 0.4%

● 12:30 PM - American - Personal Spending MoM (February)

○ Previous: 0.4%

○ Forecast: 0.6%

● 10:30 PM - New Zelander - Business NZ PMI (March)

○ Previous: 55.0

○ Forecast: 55.6

Friday 10 April

● 01:30 AM - Chinese - Inflation Rate YoY (March)

○ Previous: 1.3%

○ Forecast: 1.1%

● 12:30 PM - Canadian - Unemployment Rate (March)

○ Previous: 6.7%

○ Forecast: 6.90%

● 12:30 PM - American - Core Inflation Rate YoY (March)

○ Previous: 2.5%

○ Forecast: 2.6%

● 12:30 PM - American - Inflation Rate YoY (March)

○ Previous: 2.4%

○ Forecast: 3.1%

● 02:00 PM - American - Michigan Consumer Sentiment Prel (April)

○ Previous: 53.3

○ Forecast: 52.9

Major Earnings Reports to Watch

Wednesday 08 April

● Delta Air Lines

● Constellation Brands

Source: The Wall Street Journal, Investing, Trading Economics, Reuters, TradingView and ActivTrades’ Data as of April 3, 2026

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.