Macro is back and it's pushing micro factors to the sidelines as far as equity markets are concerned right now.

The return of big picture influence isn’t being driven by economic data, but by geo-politics and President Trump’s designs on Greenland.

When the President first remarked on Greenland it seemed as though it was a joke or throwaway comment. But just a few weeks later and the story has taken on a life of its own, as Europe lines up in support of Denmark, with President Trump threatening to introduce punitive tariffs on European imports as a punishment.

With the prospect of another trade war (or worse) in sight markets have moved to a more risk-off stance:

Risk assets such as equities are being sold, or at very least sharply marked down.

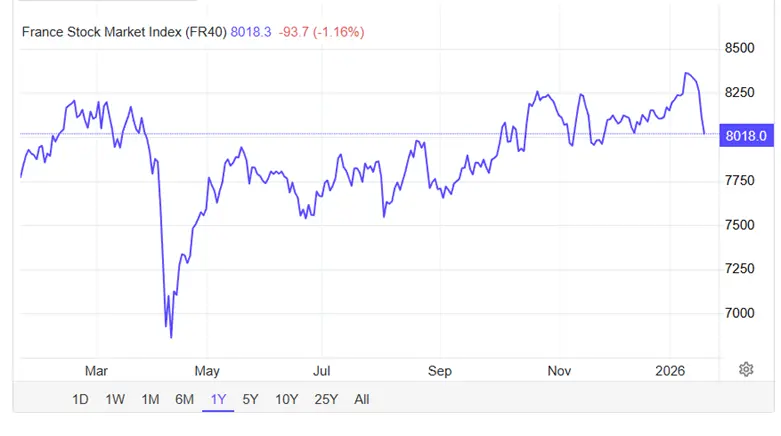

The CAC 40 index shown below, highlights what been happening over the last few days.

It’s not a full blown panic just yet

However, there are further “tank traps” on the horizon.

The World Economic Forum (WEF) holds its regular gathering in Davos this week, and President Trump is due to speak at the meeting on Wednesday afternoon (21-01-2026).

Given the tone of recent tweets and comments coming from the President, and others in his administration, it’s hard to imagine his speech will be conciliatory, and in truth he probably does hold the whip hand.

However I keep thinking ,does the US really want to damage relations with Europe( beyond repair?) by annexing Greenland?

When, with some more thoughtful negotiation it could have persuaded the Danes and Greenlanders to allow a larger US military presence in the territory. And started a discussion about access to the natural resources on the island, which covers some 2.17 million square kilometres.

Creeping up

US 10 year bond yields are creeping higher, as we can see below and they could be headed back to levels seen in the summer of 2025.

We can see the Yen strengthening against the US dollar in the chart below. That's often a sign of risk -off sentiment. The Japan 225 index has lost -2.60% in recent days, though it remains up by+ 33.74% over the last year.

Europe downgraded & Earnings overlooked

For now the market is hoping for a negotiated settlement over Greenland however Analysts at US bank Citi downgraded their outlook on European equities particularly in export led sectors such a Chemicals and Autos.Two industries that feature prominently in the German stock market.

All of this is of course over shadowing Q4 2025 earnings season which got off to mixed start its probably too early to read too much into that with only 7.0% of the S&P 500 having reported, of those a clear majority (almost 80.0%) have reported earnings above estimates, whilst 67.0% of the S&P 500 companies that have reported so far, have beaten estimates on revenues.

The blended earnings growth rate (reported earnings + estimates) for the S&P 500 stands at +8.20%. year over year and by that metric we are on course for a 10th consecutive quarter of earnings growth. But of course with 93.0% of index constituents still to release their earnings, we shouldn't put too much emphasis on that.

Commodities as a barometer

Commodity markets have been moving over the last quarter or more and it could be that they will be the best guide to how markets are interpreting rising geopolitical risks. Gold and Silver are classic safe haven plays, and Silver, which has many industrial applications, is in short supply relative to the anticipated demand for the metal.

Copper has also been moving in recent times and can act as a barometer for international trade and growth prospects.

A continued spike in gold, and to a lesser extent silver, accompanied by a downturn in copper could indicate that trade conditions are worsening, and that a flight to safety is underway.

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.