OIL

Brent oil prices hedged up during early Thursday trading, but remain close to the average price of the last two weeks, just below $80 per barrel. On the one side, prices are supported by geopolitical turbulence, with supply threatened by escalating tensions in the Red Sea and by OPEC forecasts for 2024, which predict an increase in global demand of 2.25 million bpd. However, this support has been counterbalanced by worries over slowing Chinese economic activity, a strengthening dollar, and growing US crude inventories. Against this background, the short-term outlook for the barrel price entails more of the same, with prices stuck within a relatively narrow range, between $75 and $82.

Ricardo Evangelista – Senior Analyst, ActivTrades

Source: ActivTrader

EUROPEAN SHARES

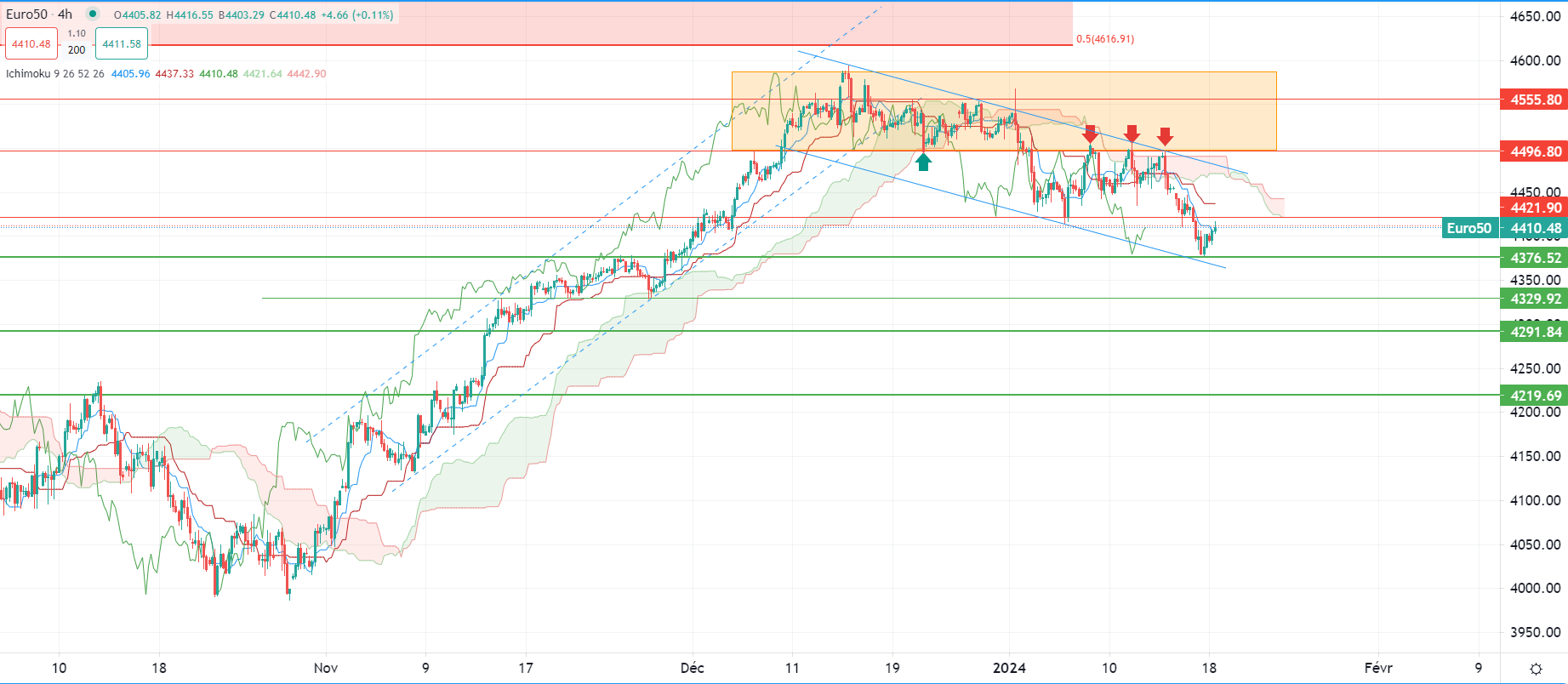

EU shares rebounded at the beginning of the trading session on Thursday, paring some of the losses registered yesterday despite uneven sectorial performances.

Bull traders managed to defend the 4,375.0pts support level on the STOXX-50 index, and prices are now headed back to the 4,420.0pts zone in a technical move to test the newly established resistance level. Performances across all sectors remain mixed as gains from consumer cyclicals and tech shares contrast with losses from all the other sectors.

We qualify today’s price action as a “technical rebound” mainly because the market recently hit a significant support level, leading short-sellers to buy back some of their positions, while the bearish macro narrative hasn’t changed.

In a further blow to bullish investors, the cautious tone from ECB and FOMC officials in Davos has also been fueled by the recent positive macro data from the US regarding retail sales, while inflation came out just as expected in the Eurozone. Again, this gives central banks the time they need to maintain their aggressive battle against inflation, delaying their dovish stance for later.

We expect even more market volatility to occur during today’s trading session as market sentiment is likely to be shaken by multiple speeches from FOMC members and ECB officials. At the same time, investors will face another slew of economic data, such as the ECB account of its monetary policy meeting, the US jobless claims, crude oil inventories and the Philadelphia Fed Manufacturing Index for January.

Pierre Veyret – Technical analyst, ActivTrades

Source: ActivTrader

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk.